A Goods and Service Tax Solution

View Combo Offer

₹7750+GST

₹00.00

- Authentication of returns through DSC/ e-sign incorporated.

- User management system for multiple logins with permitted access.

- Efficient support system to resolve all your queries / issues.

- Prepare, check and file returns in simple steps.

- Import data from Department website.

- View More

- Download 2B data for multiple months in under 2 Mins.

- Return filed/ pending. And Tally Reconciliation

- Communicate pendency to supplier and recipient via e-mail.

- Calculation of Tax Liabilities

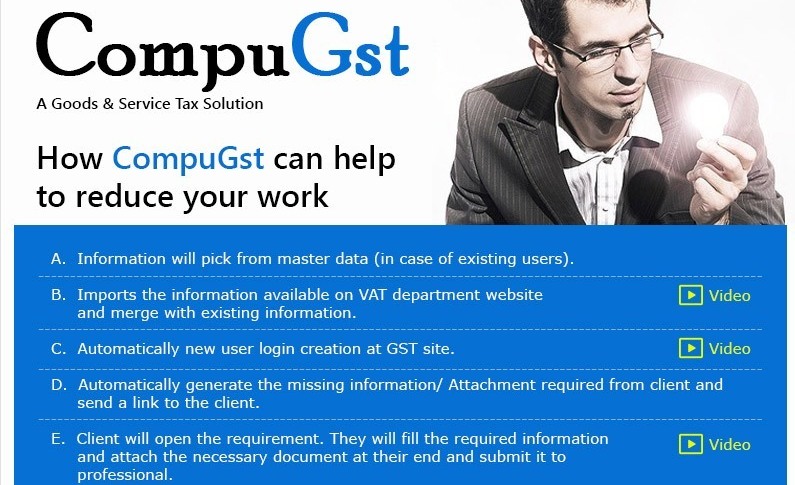

- Automatic filing of registration/ Return forms at GST site.

1 Click auto-fill GSTR 3B with GSTR-1 & 2B data.